fundamental review of the trading book

FRTB (BCBS 352) is a major regulation that impacts the Market Risk Reporting

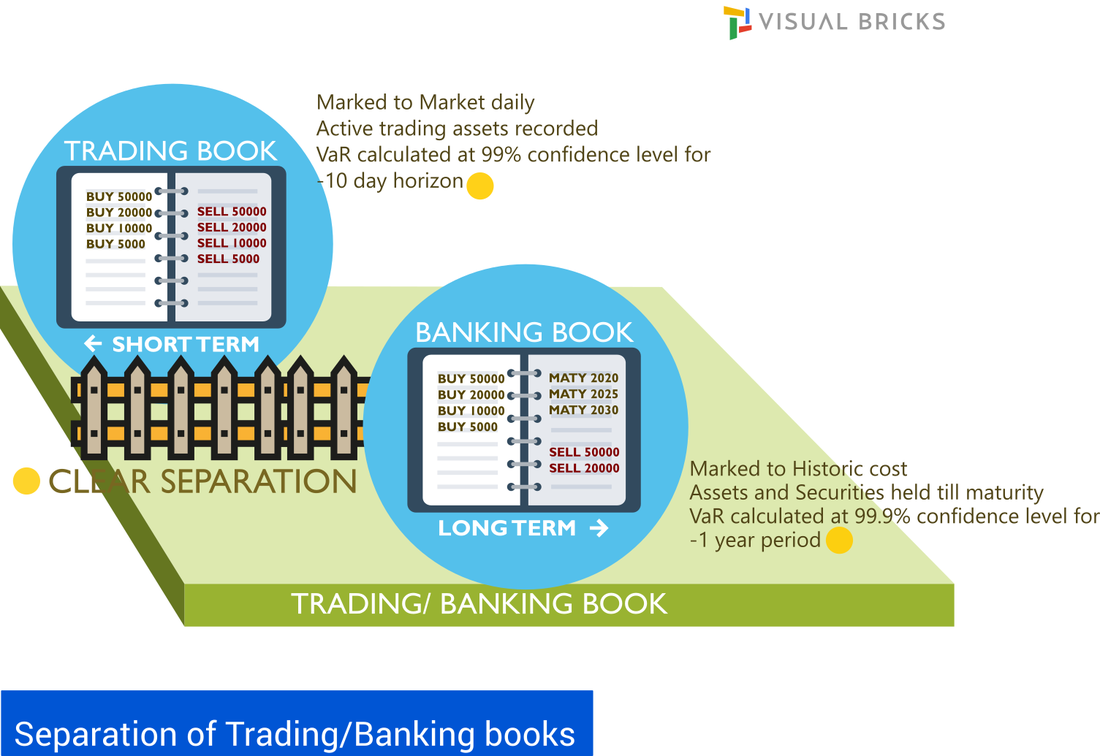

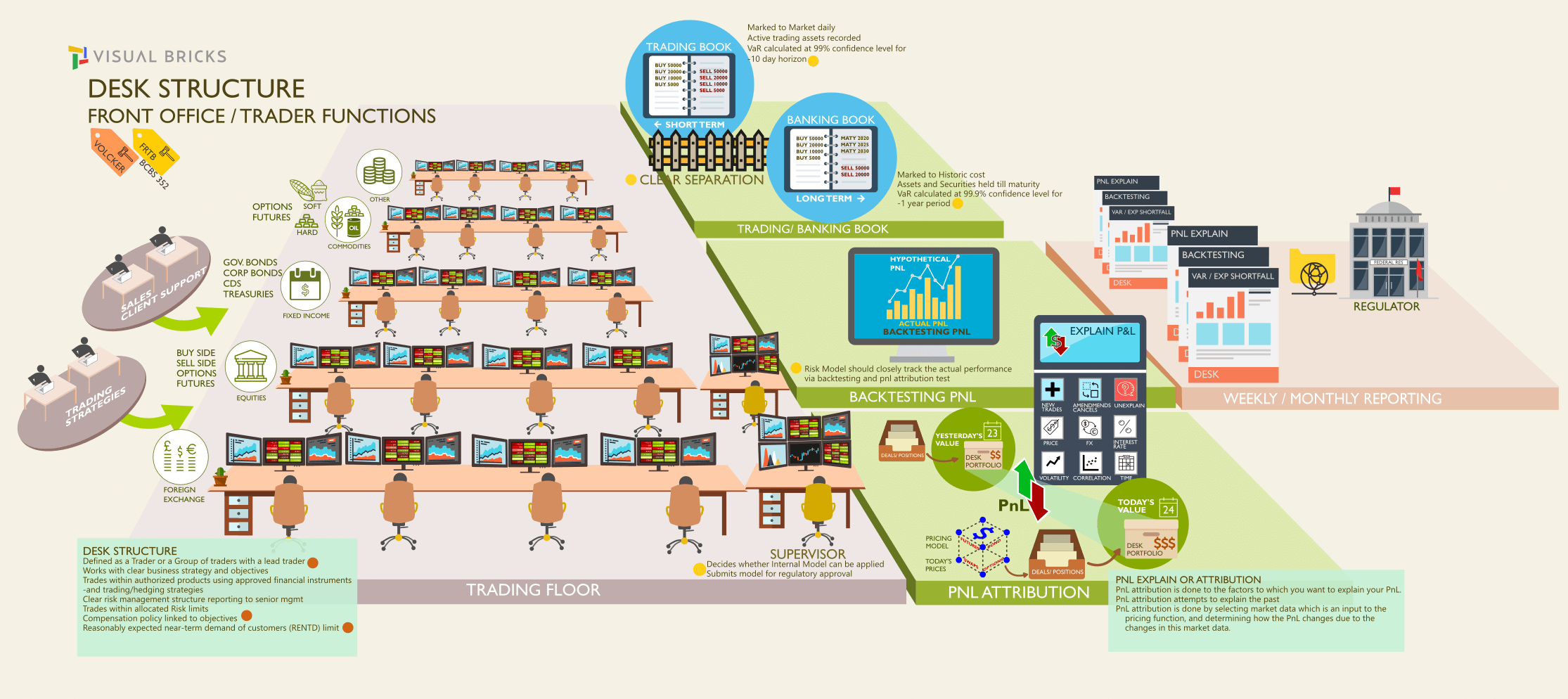

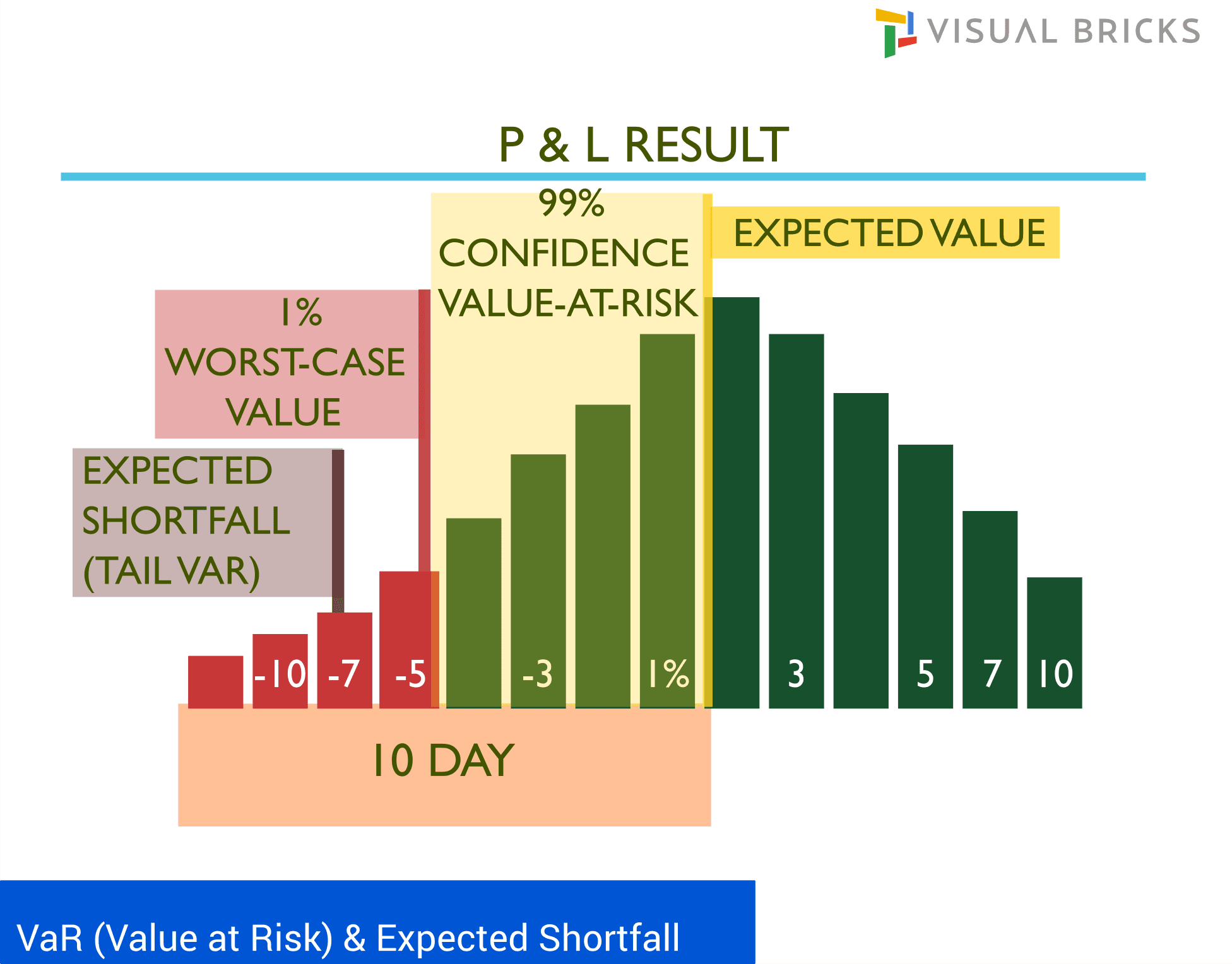

A key requirement of FRTB is the clear separation of the Trading and Banking Books. Trading books contain information and buying/selling history about all the securities currently held by the bank. All types of investment activity meant for trading is included in the trading books. Options, Futures, Currency, Commodity books are examples of different kind of books maintained by the banks. Trading book provides useful information for future trading activity and management of risk. Trading book is marked to market daily and value at risk for assets is measured on a ten day horizon under Basel II at 99% confidence level. Banking book refers to assets on banks balance-sheet that are expected to be held till maturity. Assets in the banking book are held at historic cost. The value at risk Is measured at a 99.9% confidence level on a one year horizon. Banks would hold assets in trading book to incur lower risk charge. Additionally, the new banking book / trading book boundary and its limited permeability in terms of internal risk transfers may put entire trading strategies and business lines at risk due to higher capital costs. |

|

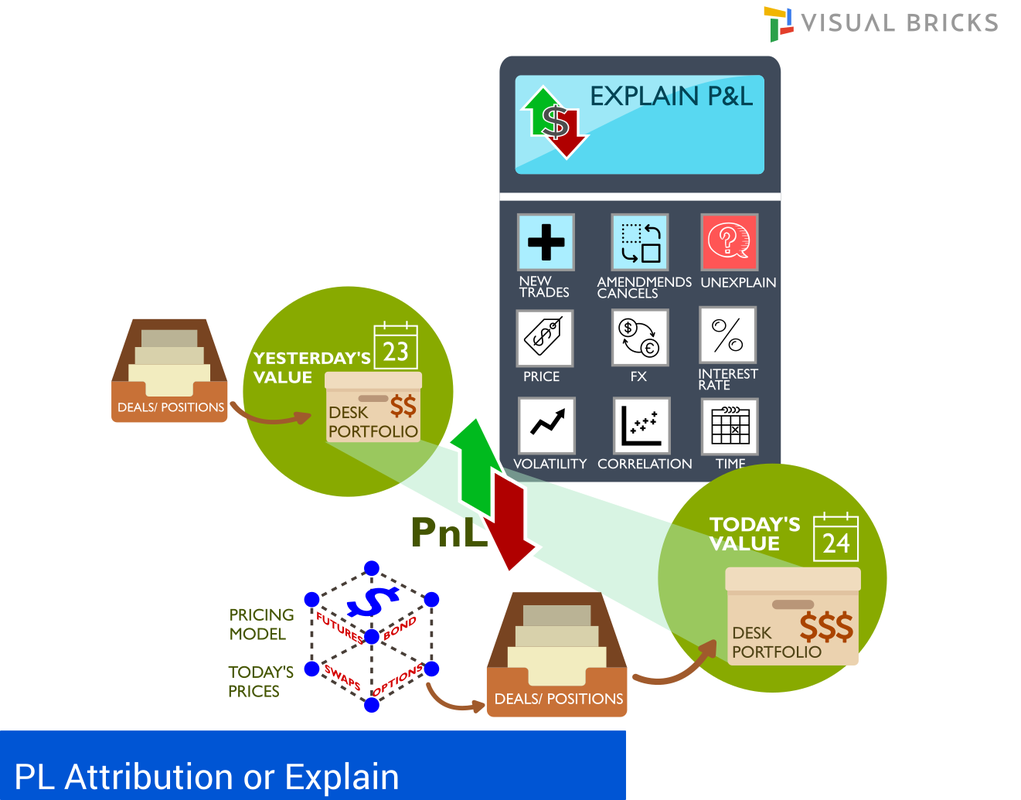

PnL attribution PnL = Value of portfolio as of today - Value of Portfolio as of yesterday. PnL attribution gives you that information on what generated that PnL. It is done to factors. 100% of PnL is explained to the factors, whatever remains unattributed is assigned to "Unexplained". Sensitivities are computed to the factors which is used to predict the PnL. P&L attribution reporting is based on two metrics and is reported prior to end of every month:

|

|

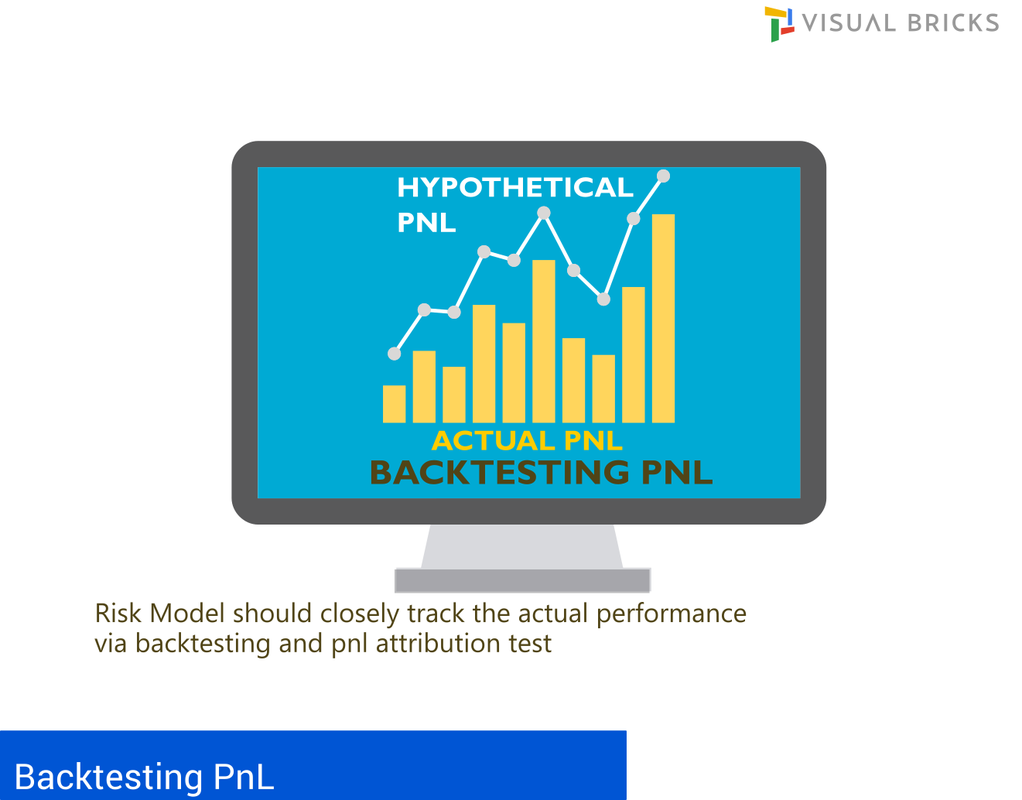

Backtesting Actual pnl is compared to the hypothetical pnl calculated using the front office pricing models which contains more risk factors and is more precise. Risk models should closely track the actual performance vis backtesting and the PnL attribution test. Risk theoretical pnl for a desk is based on the firms risk management models and are not based on front office pricing models. Backtesting requires comparing each desk’s 1-day static var at both the 97.5th percentile and the 99th percentile, using at least one year of current observations of the desk’s one-day P&L. If any given desk experiences either more than 12 exceptions at the 99th percentile or 30 exceptions at the 97.5th percentile in the most recent 12-month period, all of its positions must be capitalised using the standardised approach until the desk no longer exceeds the above thresholds over the prior 12 months. |

|

|

Expected shortfall must be computed on a daily basis at a 97.5th percentile confidence level for each trading desk included in the scope for the internal model. The calculation must be calculated for a base liquidity horizon of 10 days and scaled to 20,40,60 and 120 days liquidity horizon. The horizons are based on risk factor categories. The ES must be calibrated to a the most severe 12-month period of stress over the observation horizon in which the portfolio experienced the largest loss using relevant risk factors.

Models must be periodically revalidated for any structural changes in market or the composition of the portfolio. If the desk experiences four or more breaches within the prior 12 months then it must be capitalised under the standardised approach. Banks must calculate the standardised capital charge for each trading desk which will be used as fallback capital charge for those desks that fail the eligibility under internal model approach. |

|